This page serves as a complete reference for the official electronic invoicing calendar 2026–2027, with a breakdown by company size and type of obligation (receipt, emission, e-reporting).

Mandatory electronic invoicing represents one of the most significant regulatory changes for French companies in decades. Starting in 2026, and more broadly in 2027, all companies subject to VAT must issue and receive invoices according to strict requirements, with standardized formats and transmission channels governed by the State. This reform, detailed in our comprehensive guide to electronic invoicing, goes far beyond a simple regulatory deadline: it fundamentally transforms financial, accounting, and procurement processes.

One of the most sensitive and often misunderstood points concerns the official obligations calendar. Who must be ready in 2026? Who can wait until 2027? What is the difference between receipt obligation and emission obligation? And most importantly, what does being “ready” by a given date actually mean?

Contrary to popular misconception, the reform does not apply to all companies at the same time. The legislature has planned a phased rollout, taking into account the size of organizations and their capacity to absorb this change. However, this phased approach should not be confused with an absence of urgency.

On this page, we offer you a clear and actionable breakdown of the electronic invoicing obligations calendar 2026/2027: key dates, companies concerned, differences between e-invoicing and e-reporting, and concrete impacts for your organization. To delve deeper into technical aspects, you can also consult our dedicated page on electronic invoice formats accepted in France.

The goal is simple: to enable you to know when to act, what to act on, and why to get ahead.

Why a progressive schedule for electronic invoicing?

Mandatory electronic invoicing could not be deployed uniformly and immediately across all French companies. The State therefore chose a progressive schedule, spread between 2026 and 2027, to ensure adoption of the system without disrupting economic actors.

The first reason is the diversity of companies involved. Between a microenterprise and a large international group, the levels of tooling, digital maturity, and internal resources are very different. Imposing the same deadlines on everyone would have created a high risk of non-compliance, invoicing flow blockages, and payment delays.

The second reason lies in the profound transformation of processes. Electronic invoicing is not simply about changing the invoice format. It requires reviewing the circuits for emission, reception, control, archival, and transmission of tax data. A progressive rollout allows companies to test, adjust, and secure these new flows before generalization.

Finally, this staggered schedule addresses a macroeconomic and fiscal challenge. The objective of the reform is also to strengthen the fight against VAT fraud and improve the quality of economic data transmitted to the administration. A progressive deployment ensures the system scales up effectively, both from the perspective of companies and approved platforms and State systems.

This phasing is therefore not a grace period, but a time for strategic adaptation. Companies that anticipate now have a major operational advantage when their obligations actually come into effect.

Key dates of the reform (overview)

The e-invoicing reform follows a precise and staggered schedule, defined by the administration to progressively structure the rollout of the system. Understanding these key dates is essential to anticipate your obligations, organize your internal projects, and avoid last-minute compliance efforts.

Implementation in two phases: reception then emission

The schedule is based on a simple logic:

all companies must first be able to receive electronic invoices, before being gradually required to issue them.

This approach secures incoming flows before generalizing outgoing flows, which are often more complex to manage.

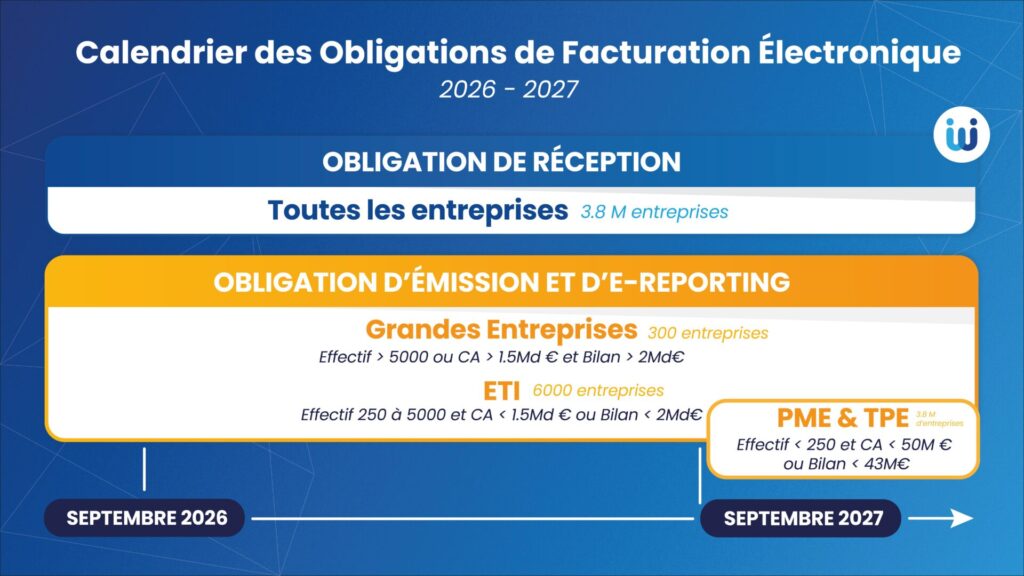

September 1, 2026: a pivotal date for all companies

From September 1, 2026:

-

All companies subject to VAT, regardless of size, must be able to receive electronic invoices through the official channel (approved platform).

-

At that same date, the obligation to issue electronic invoices will come into effect for:

-

large enterprises,

-

mid-sized enterprises (MTEs).

-

This is therefore a major milestone that affects the entire French economic landscape, at least on the reception side.

September 1, 2027: generalization of emission

On September 1, 2027, the second major phase of the reform begins. On this date, the obligation to issue electronic invoices will extend to:

-

SMEs,

-

microenterprises.

From that moment forward, all companies subject to VAT will be subject to both:

-

the reception obligation,

-

the obligation to issue electronic invoices.

A schedule to read as a trajectory, not as a simple deadline

These dates should not be interpreted as isolated starting points, but as stages of a transformation trajectory. The sooner a company plans the restructuring of its processes, the choice of its formats and tools, the smoother the transition will be when the obligation becomes effective.

The schedule provides a framework. Performance depends on preparation.

| Company Size | Mandatory Reception | Mandatory Emission |

|---|---|---|

| All companies | September 2026 | — |

| Large enterprises | September 2026 | September 2026 |

| MTE | September 2026 | September 2026 |

| SMEs | September 2026 | September 2027 |

| Microenterprises | September 2026 | September 2027 |

2026: first mandatory requirements (what really begins)

The year 2026 marks the true operational turning point of the electronic invoicing reform. Until now, businesses could prepare, test, and anticipate. Starting in September 2026, obligations become concrete, enforceable, and structuring for all economic actors.

A universal obligation to receive electronic invoices

From September 1, 2026, all VAT-registered companies must be able to receive electronic invoices, with no exception based on size or sector.

Concretely, this means:

-

having an official reception point via an approved platform,

-

being able to receive invoices in one of the authorized formats (Factur-X, UBL or CII),

-

integrating these invoices into your accounting and financial processes.

Even companies that issue very few invoices must therefore be technically ready to receive compliant electronic flows.

Beginning of the issuing obligation for large structures

The same date also marks the start of the issuing obligation for:

-

large enterprises,

-

mid-sized companies (ETI).

These companies must now issue their B2B invoices exclusively in electronic form, via the official channel and in a structured format recognized by the tax authorities.

This notably requires:

-

tools capable of generating compliant electronic invoices,

-

stabilized internal processes (reference data, VAT, orders),

-

clear organization of flows between systems, platforms and partners.

E-reporting: an obligation often underestimated

2026 also marks the effective start of e-reporting for certain transactions, notably:

-

B2C transactions,

-

international operations,

-

certain flows not subject to B2B electronic invoicing.

E-reporting requires the transmission of transaction data to the tax authorities, even when there is no electronic invoice in the strict sense. This is a separate topic, but closely linked to the reform, and often more complex than it appears.

2026: a year of organizational strain

In practice, 2026 is the year when preparation gaps become visible.

Companies that have anticipated will see their flows stabilize.

Those that have waited will be exposed to:

-

invoice rejections,

-

payment delays,

-

friction with their partners,

-

and increased pressure on finance and IT teams.

The reform does not begin in 2026.

👉 It is revealed in 2026.

2027: Generalization of the issuing obligation

After the entry into force of the first obligations in 2026, 2027 marks the completion of the rollout of mandatory electronic invoicing. From that date, all companies affected by the reform must not only be capable of receiving electronic invoices, but also issue them systematically as part of domestic B2B exchanges.

Extension of the issuing obligation to all companies

Starting from September 1st, 2027, the obligation to issue electronic invoices is extended to:

-

small and medium enterprises (SMEs),

-

micro-enterprises,

-

more broadly, all companies subject to VAT that were not affected by the issuing obligation in 2026.

In other words, company size is no longer a differentiating criterion. From that date, every B2B invoice issued in France must necessarily:

-

be issued in electronic form,

-

use an authorized structured format (Factur-X, UBL or CII),

-

transit through the official electronic invoicing channel via an approved platform.

The PDF sent by email disappears definitively from compliant practices.

A reform fully operational across the entire economic landscape

With this generalization, the reform achieves its main objective:

👉 standardize all B2B invoicing flows, regardless of the actors involved.

This means that:

-

relationships between large corporations and SMEs are fully aligned,

-

suppliers of all sizes must adapt,

-

invoicing chains become homogeneous and traceable.

For the least equipped companies, 2027 often represents the true turning point, as issuing electronic invoices requires:

-

compliant generation tools,

-

reliable data (customers, VAT, line items),

-

clear organization of invoicing processes.

2027: less a novelty than a confirmation

Unlike 2026, 2027 does not introduce new rules, but confirms their generalized application. Companies that have properly anticipated in 2026 will benefit from continuity.

Conversely, those that have postponed compliance will have to absorb, in a short time:

-

technical changes,

-

organizational adaptations,

-

and increased pressure from their customers and partners who are already compliant.

2026: mandatory reception for all, issuance for large corporations and mid-sized companies

2027: mandatory issuance for all companies

Electronic Invoicing vs E-Reporting: Different Timelines

The 2026–2027 reform groups together two distinct obligations, often confused:

the electronic invoicing and e-reporting.

While they are linked on a regulatory level, their scopes and timelines are not strictly identical. Understanding this difference is essential to avoid misinterpretation errors… and preparation mistakes.

Electronic Invoicing: Domestic B2B Transactions

Electronic invoicing concerns exclusively B2B transactions conducted between French companies subject to VAT.

It requires:

-

the issuance and receipt of invoices in a structured format (Factur-X, UBL or CII),

-

passage through an approved platform,

-

transmission of invoicing data to the authorities via the Public Invoicing Portal (PPF).

Its timeline is progressive:

-

Receipt mandatory for all companies from September 1, 2026,

-

Issuance mandatory in 2026 for large companies and mid-cap enterprises,

-

Generalized issuance in 2027 for SMEs and micro-enterprises.

E-Reporting: Transactions Outside the Mandatory B2B France Scope

E-reporting, for its part, applies to operations that do not fall under mandatory electronic invoicing, in particular:

-

sales to individual customers (B2C),

-

international transactions (exports, intra-community),

-

certain specific operations not subject to electronic invoicing.

In these cases, there is not always an electronic invoice transmitted via a platform, but the company must report transaction data to the tax authorities.

An Aligned Timeline… But Not Identical

Even though e-reporting starts in the same period as electronic invoicing, its timeline is closely linked to that of issuance, not receipt.

Concretely:

-

companies affected by e-reporting must submit their data when they become subject to the issuance obligation,

-

the scope of e-reporting depends therefore on the type of operations performed, not solely on company size.

Why This Distinction Is Strategic

Confusing electronic invoicing and e-reporting often leads to:

-

underestimating actual obligations,

-

delaying compliance on certain transactions,

-

improperly sizing tools and platforms.

Conversely, clearly distinguishing the two allows:

-

structuring a realistic roadmap,

-

identifying precisely the affected flows,

-

avoiding unpleasant surprises during the first audits.

Electronic invoicing and e-reporting move forward together, but do not follow the same logic.

Mastering them separately is a key condition for lasting compliance.

What the calendar means in practice for your organization

The 2026/2027 electronic invoicing calendar should not be read as a mere succession of regulatory dates. It involves concrete structural changes in the organization of finance, procurement, and IT processes, well ahead of the official deadlines.

Mandatory reception from 2026: immediate impact for all

From September 1, 2026, all VAT-registered companies must be able to receive electronic invoices, regardless of their size.

Specifically, this means your organization must:

-

have a declared reception point (via an approved platform),

-

be able to read, store, and trace invoices in structured formats (Factur-X, UBL, CII),

-

integrate these invoices into your accounting and control processes.

👉 Even if you are not yet issuing electronic invoices, your suppliers can send them to you. Not being ready to receive them exposes you to operational blockages (unintegrated invoices, payment delays, disputes).

Progressive emission: a deeper transformation than it appears

The emission requirement, which is staggered between 2026 and 2027 depending on company size, involves far more than a simple format change.

It requires:

-

reviewing your invoicing tools (ERP, accounting software, third-party solutions),

-

structuring and strengthening your invoicing data (customers, VAT, lines, references),

-

choosing a suitable format for your maturity level (Factur-X, UBL or CII),

-

integrating transmission via an approved platform, with status and feedback management.

👉 Electronic emission often reveals existing flaws: incomplete data, manual processes, late controls.

Direct impact on internal processes

The calendar acts as a transformation accelerator:

-

invoices can no longer be corrected “after the fact”,

-

errors are detected earlier and block workflows,

-

exchanges become more standardized and traceable.

This requires better coordination between:

-

finance and accounting,

-

procurement and suppliers,

-

IT and solution providers.

Why waiting would be a mistake

Companies that approach the reform only from a compliance angle take a risk:

-

projects carried out in haste,

-

forced technical choices,

-

additional costs and organizational rigidity.

Conversely, anticipating the calendar allows you to:

-

spread efforts over time,

-

align electronic invoicing with Procure-to-Pay,

-

transform a regulatory obligation into a lever for reliability and financial control.

👉 The calendar is not just a legal constraint: it is a transformation framework that durably impacts your organization.