2026 marks a decisive turning point for all French companies. The reform of electronic invoicing, orchestrated by the tax administration, is not a simple evolution; it is a profound transformation of working methods, tools, and interactions between economic actors. This ambitious initiative, which aims to modernize exchanges, improve VAT control, and reduce tax fraud, is part of a structured and progressive regulatory framework.

At the heart of this reform, two concepts recur constantly, often used interchangeably, but covering distinct realities and specific obligations: e-invoicing and e-reporting. This confusion, frequent and understandable, constitutes nevertheless one of the main sources of poor anticipation of the reform, leading to delays in compliance and significant operational risks. From the complexity of the timeline to the specifics of the flows involved, understanding the distinction between these two pillars is the first step toward a smooth and successful transition.

This expert article from Weproc aims to demystify electronic invoicing for 2026 by detailing precisely what e-invoicing and e-reporting are. We will explore their definitions, their fields of application, the types of transactions they cover, as well as their concrete impacts on your organization. Our goal is to provide you with a clear roadmap, free of superfluous jargon, to enable you to anticipate upcoming deadlines and guarantee essential compliance for your company.

⏱️ The Essential in 2 Minutes

- E-invoicing concerns domestic B2B invoices, transmitted in structured format via certified platforms.

- E-reporting is the obligation to transmit transaction data (B2C, international) to the tax administration, without issuing a complete invoice.

- These are two distinct but complementary obligations, stemming from the same reform to optimize VAT management.

- All companies will be impacted, first in receipt from September 2026, then progressively in emission and for e-reporting according to their size.

- Anticipation requires a structured approach and can rely on distinct but interoperable tools, notably a Procure-to-Pay solution to reliabilize receipt.

Understanding the Challenge: Why Is This Confusion Frequent?

The confusion between e-invoicing and e-reporting is not fortuitous. It results from a set of factors that, taken individually, seem logical, but that, combined, create interpretive complexity for companies. Unraveling these origins is the first step toward a clear understanding of the reform.

The Common Objective and Shared Regulatory Origins

One of the main reasons for this confusion lies in the macroeconomic objective shared by both mechanisms. The electronic invoicing reform, as a whole, aims at both a modernization of commercial exchanges, a strengthening of the fight against VAT fraud, and an improvement of knowledge about economic activity in real time. These common objectives are enshrined in the same legislative and regulatory texts, notably the finance law for 2020, which laid the foundations for this transformation.

Moreover, the deployment of both obligations relies on common technological infrastructure: the Public Invoicing Portal (PPF) and Certified Platforms (PA). These actors play a central role in the transmission of electronic invoices (e-invoicing) and transaction data (e-reporting), which reinforces the impression of unified management of flows. For many companies, the idea that the same system can manage all tax information naturally leads to thinking that it is a single obligation.

The Ambiguity of Administrative Vocabulary

The language used in official communications can also perpetuate ambiguity. Terms such as “electronic invoicing,” “data transmission,” “declaration,” or “reporting” are sometimes used interchangeably, without always an explicit distinction between issuing a complete invoice and simply sending key information to the administration. This semantic imprecision, though often unintentional, sows doubt and makes it difficult for non-experts to grasp the precise contours of each obligation.

For example, a company that sells products abroad might be tempted to think it is fully compliant if it already manages e-invoicing for its French customers, while its international operations specifically fall under e-reporting. The absence of a perfectly distinct nomenclature in public discourse thus has a direct impact on companies’ ability to organize themselves effectively.

The Risks of Poor Anticipation

The consequences of a misunderstanding between e-invoicing and e-reporting can be severe. First, it can lead to delays in compliance. If a company does not realize it is subject to both obligations, it risks focusing solely on one of them, neglecting the other until the last minute.

Next, poor anticipation can lead to inadequate tool selection. A supposedly “all-in-one” solution could prove insufficient to manage the combined complexity of both flows, or conversely, a company might invest in oversized systems due to ignorance of real perimeters.

Finally, the most critical risk is that of penalties. Non-compliance with electronic invoicing obligations can lead to significant fines, as provided for by the General Tax Code. Beyond financial sanctions, a non-compliant company faces ruptures in its payment chain, disputes with suppliers and customers, and a degradation of its reputation. Clarifying these concepts now is therefore not an option, but a strategic necessity for any company operating on French territory.

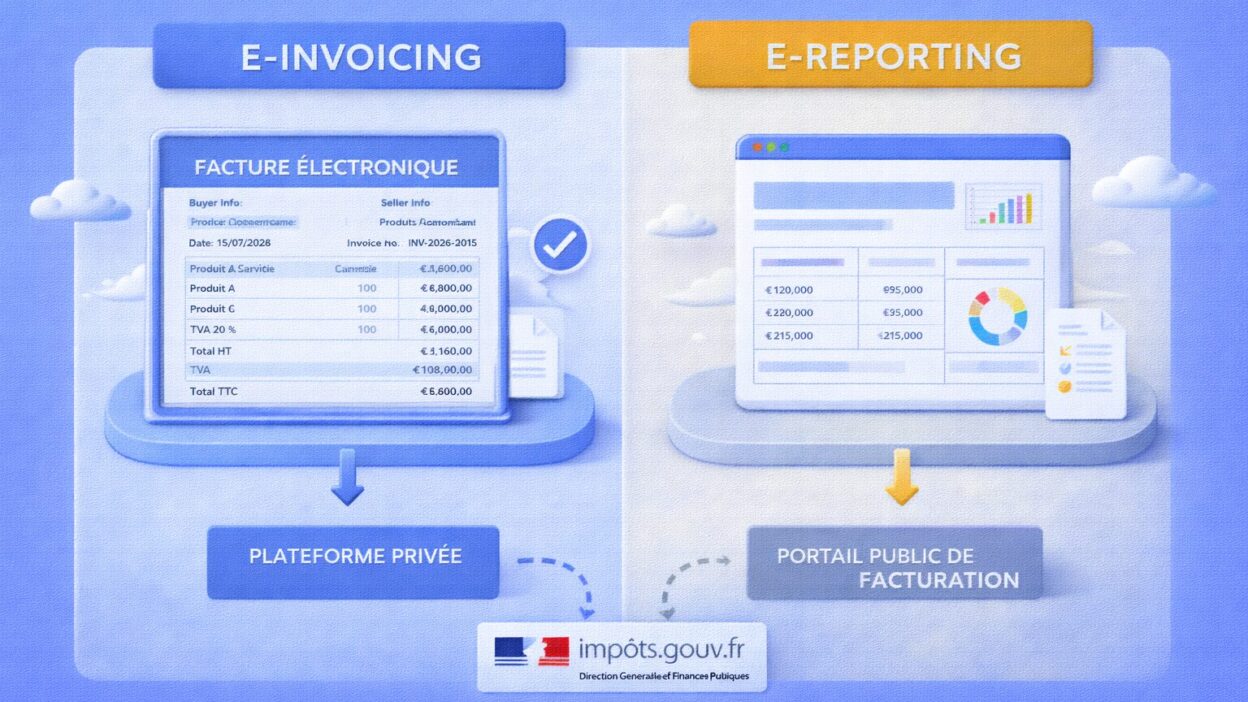

E-invoicing: Electronic Invoicing for Domestic B2B Exchanges

The term e-invoicing, or electronic invoicing, is at the heart of the 2026 reform. It designates a precise obligation, governed by law, that will transform the way companies issue, transmit, and receive their invoices.

Definition and Exclusive Domestic B2B Perimeter

E-invoicing is defined as the obligation to issue, transmit, and receive invoices in a structured electronic format, according to a regulatory framework defined by the State. It is crucial to understand that an electronic invoice within the meaning of the reform is not a simple PDF document sent by email. It is a file whose data is structured in such a way as to be readable and automatically exploitable by computer systems, on the side of both the issuer and the receiver, and of course by the tax administration.

The scope of e-invoicing is clear and exclusive: it applies only to domestic B2B transactions. This means it applies to invoice exchanges between two French companies subject to VAT. Sales to individuals (B2C) and international transactions (exports, imports, intra-community deliveries, or services provided abroad) are explicitly excluded from this mechanism and fall under another obligation, e-reporting, which we will address later. This precision is fundamental for determining which invoices are concerned and how they should be handled.

Standardized Electronic Formats: Factur-X, UBL, CII

To ensure interoperability and process automation, the tax administration has defined a list of accepted electronic formats. These formats are not mere data containers; they structure information in such a way that it is universally understandable and processable by computer systems. The three main recognized formats are:

- Factur-X: This is a hybrid format, combining a PDF file readable by humans and an embedded XML file containing structured data. It is an excellent compromise, as it allows immediate visualization while guaranteeing automatic data exploitability. Factur-X is particularly suitable for SMEs that wish to maintain a visual approach while complying.

- UBL (Universal Business Language): This format is a purely structured international XML standard. It is intended for the automatic exchange of commercial documents and is widely used in ERP systems and e-procurement solutions. It offers great data richness and advanced automation.

- CII (Cross Industry Invoice): Another structured XML format, CII is also an ISO standard. It is characterized by its robustness and its ability to handle complex scenarios of inter-industry data exchanges.

The choice of format will depend on the company’s size, its invoicing volumes, and the sophistication of its information system. The essential is to choose a format that guarantees reliable reading by accounting systems, automated reconciliation, and secure archiving.

The Transmission Circuit via Certified Platforms

E-invoicing goes beyond simple format: it imposes a new transmission circuit. No more sending invoices directly between supplier and customer by email or mail. From now on, each B2B invoice must pass through an approved intermediary, either a Certified Platform (PA) or the Public Invoicing Portal (PPF).

The process typically unfolds as follows:

- The supplier issues its invoice in a standardized electronic format (Factur-X, UBL, CII).

- It transmits this invoice to its PA (Certified Platform) or directly to the PPF if it chooses this route (“Public Portal only” mode).

- The supplier’s PA performs compliance checks on the invoice and extracts key data (amount, VAT, identification of parties).

- This data is transmitted to the PPF, which then relays it to the tax administration.

- The complete invoice is routed by the PPF to the customer’s PA or directly to the customer if they have chosen the PPF as their reception method.

- The customer receives the invoice via their PA or the PPF and integrates it into their system.

This supervised circuit guarantees the security, integrity, and authenticity of invoices, while providing the administration near real-time visibility into commercial flows. E-invoicing transforms the invoice into a true standardized and traceable data flow, essential to the new B2B invoicing model in France.

E-reporting: Data Transmission for Other Flows

While e-invoicing captures attention through its visible nature of “electronic invoice,” e-reporting is the second building block, often less publicized but equally fundamental, of the 2026-2027 electronic invoicing reform. Its role is to complement the mechanism for all operations that do not fall within the strict scope of domestic B2B e-invoicing.

Definition: Data Transmission, Not Invoice

Unlike e-invoicing, which imposes the issuance and transmission of a complete invoice in structured format, e-reporting consists of the obligation to transmit to the tax administration transaction data for certain operations. It is not a matter of sending a complete invoice to the customer or the administration, but of declaring key information, extracted from sales or receipts, via the official electronic invoicing channel. In other words, the nature of the transaction does not imply an electronic invoice in the strict sense (which is not always required or whose format is not structured for the reform), but the State needs to know its details for its tax control objectives. This distinction is crucial: e-reporting = data transmission, not invoice transmission.

The Operations Concerned: B2C, International, and Other Specific Flows

E-reporting takes over where e-invoicing stops. It concerns a broad range of operations that, by their nature, are not domestic B2B transactions. The most frequent cases include:

- Sales to individuals (B2C) with VAT: Whether it is a store sale, online sale, or a service provided to a non-professional, the data of these transactions must be transmitted to the administration.

- International operations: This encompasses exports of goods and services (sales outside France), intra-community deliveries (sales to professionals in other EU countries), and services provided to or from abroad. These flows, although not subject to French e-invoicing, are essential for monitoring international VAT.

- Certain specific operations outside the scope of mandatory electronic invoicing: These may be transactions for which invoicing is not mandatory (for example, restaurant receipts for business meals), but whose data may be relevant to the tax administration.

It is therefore very common for a company to be subject simultaneously to e-invoicing for its French B2B invoices and to e-reporting for a part, sometimes the majority, of its other business flows. Ignoring one of these aspects is ignoring a significant portion of its obligations.

The Types of Data Transmitted and the Circuit

The information to be transmitted as part of e-reporting is targeted and essential for tax monitoring. It concerns mainly:

- The identification of the issuing company.

- The date of the operation or receipt (depending on the applicable VAT regime).

- The total amount of the transaction, broken down before taxes.

- The amount of VAT collected, detailed by rate.

- The nature of the operation (sale of goods, service provision, receipt).

- The type of customer (individual or foreign professional) and their country.

This data is generally aggregated and transmitted periodically (for example, daily or monthly) via the Certified Platform (PA) chosen by the company, or directly via the Public Invoicing Portal (PPF). The PAs will play a key role in collecting, validating, and securely transmitting this information to the PPF, which will then centralize it for the tax administration. It is crucial to consult the official list of Certified Platforms to choose the right partner.

The Direct Link with VAT and Tax Management

E-reporting is intrinsically linked to the tax objective of the reform. It enables the administration to pre-fill companies’ VAT declarations and cross-reference information to more effectively detect anomalies and fraud. For companies, this implies a major change: the collection and declaration of sales data will no longer be done solely a posteriori via the VAT declaration, but much more regularly and granularly. It is a true paradigm shift in the relationship between the company and the tax administration, offering increased transparency and reliabilization of national and international economic data.

Although less “visible” than invoice management, e-reporting requires rigorous discipline on the quality, consistency, and timeliness of VAT data transmission. This is why its underestimation can lead to non-negligible operational and tax complications.

E-invoicing vs E-reporting: The Comparative Summary Table

To dispel any ambiguity and consolidate your understanding, the most effective way is to directly confront e-invoicing and e-reporting on their fundamental characteristics. These two pillars of the electronic invoicing reform share a common objective, but differ radically in their application, scope, and the nature of information transmitted.

| Comparison Axis | E-invoicing (Electronic Invoicing) | E-reporting (Data Transmission) |

|---|---|---|

Type of Operations |

Domestic B2B transactions (between French companies subject to VAT). | Transactions outside B2B France (B2C, export, intra-community, other specific operations). |

| Concrete Examples | Sale of merchandise between a French wholesaler and a French retailer. | Online sale to an individual, export of goods to Canada, service provision to a German company. |

Nature of Transmission |

Transmission of a complete electronic invoice (structured data + readable). | Transmission of key data only, aggregated or not, without the entire invoice. |

| Content Transmitted | Structured invoice (lines, amounts, VAT, references, complete legal information). | Transaction and/or receipt data (amount before/after tax, VAT, date, operation type, issuer/recipient ID). |

| Formats Involved | Factur-X, UBL, CII (formats recognized by the administration). | Structured data according to a schema defined by the State, often via XML or API. |

Recipients and Objectives |

The customer receives the complete invoice; the tax administration receives the invoice data. Dual objective: commercial exchange + tax control. | The tax administration only receives the data. Single objective: VAT management, fraud prevention, economic knowledge. |

| Transmission Circuit | Supplier’s platform → Customer’s platform → PPF (for administration data). | Company’s platform → PPF (for administration data). |

| Obligation (from Sept. 2026) | Mandatory receipt for all companies; mandatory emission for Large Enterprises and Mid-Size Companies. | Begins for companies conducting relevant operations (Large Enterprises, Mid-Size Companies first). |

| Generalization (Sept. 2027) | Mandatory emission for all companies (SMEs and Micro-enterprises included). | Extended to all companies conducting relevant operations (SMEs, Micro-enterprises included). |

What Must Be Remembered from the Comparison

This table highlights the complementary nature of e-invoicing and e-reporting. The first is concerned with the dematerialization and circulation of invoices between VAT-registered professionals in France. The second fills the gap for all other operations, ensuring that the tax administration has a comprehensive view of economic activity, regardless of the nature of the customer or the location of the transaction.

The most costly error would be to consider that one of these obligations replaces the other, or that a company is subject to only one of the two. In reality, a majority of French companies will be subject to both mechanisms, simultaneously or progressively. Mastering this distinction is not only a compliance imperative, but also a prerequisite for selecting the right tools, adapting internal processes, and training teams accordingly. Compliance with electronic invoicing in 2026-2027 depends on the combined mastery of these two flows, depending on the reality of your commercial transactions.

Timeline 2026-2027: Who Is Concerned and When?

The implementation of electronic invoicing is progressive, an approach aimed at giving companies the necessary time to adapt. However, the distinction between e-invoicing and e-reporting, and the deadlines specific to each, requires particular attention. Understanding this timeline is fundamental for planning your transition without rushing.

September 2026: The Launch of the Reform

September 1, 2026 marks the first major stage of the reform, with differentiated obligations according to company size and role:

- Mandatory receipt obligation for all companies: From this date, regardless of their size (micro-enterprise, SME, Mid-Size Company, Large Enterprise), all VAT-registered companies must be able to receive electronic invoices compliant with e-invoicing. This means they must have selected their dematerialization platform (PA or PPF) and configured their systems to process these incoming flows. The objective is to guarantee flow smoothness from the start, allowing issuing companies not to be blocked by unprepared customers.

- Mandatory emission obligation for Large Enterprises and Mid-Size Companies (ETI): The largest companies, defined by legal thresholds (turnover, workforce), will be the first required to issue their domestic B2B invoices in electronic format via approved platforms. This is a significant technical and organizational challenge for these structures, which often must adapt complex information systems and high invoicing volumes.

- Start of e-reporting for concerned companies: Parallel to e-invoicing, the e-reporting obligation also begins September 1, 2026 for the same categories of companies (Large Enterprises and Mid-Size Companies) that conduct operations outside B2B France (B2C sales, international transactions). These companies must begin transmitting data for these transactions to the tax administration via their platforms.

September 2027: Generalization

The second wave of the reform will occur on September 1, 2027, with the extension of obligations to smaller companies:

- Generalization of B2B emission for all companies: On this date, Small and Medium-Sized Enterprises (SMEs) and Micro-enterprises subject to VAT will join Large Enterprises and Mid-Size Companies in the obligation to issue their domestic B2B invoices in electronic format. This is a crucial stage that will encompass virtually the entire French economic fabric.

- Extension of e-reporting to all SMEs and Micro-enterprises: Similarly, SMEs and Micro-enterprises that conduct operations falling under e-reporting (B2C, international) must, from September 2027, transmit this data to the tax administration.

This progressive timeline should not be interpreted as a sign that preparation can be postponed. On the contrary, it underscores the importance of anticipation. Even the smallest companies, while benefiting from an additional year of delay for emission, must be ready from 2026 to receive electronic invoices and begin evaluating their e-reporting needs. The complexity often lies in updating internal systems, training teams, and selecting reliable partners.

To better visualize the chronology, here is a diagram of the deployment process:

Electronic Invoicing Deployment Process

September 1, 2026

- Phase 1: General Receipt

- • All companies: Mandatory receipt of electronic invoices (e-invoicing).

- Phase 2: Emission & Initial E-reporting

- • Large Enterprises (GE): Mandatory emission e-invoicing & e-reporting start.

- • Mid-Size Companies (ETI): Mandatory emission e-invoicing & e-reporting start.

September 1, 2027

- Phase 3: Complete Generalization

- • Small and Medium-Sized Enterprises (SMEs): Mandatory emission e-invoicing & e-reporting generalization.

- • Micro-enterprises: Mandatory emission e-invoicing & e-reporting generalization.

This timeline highlights the progressive yet determined approach of the administration for the generalization of electronic invoicing.

Anticipation is the key to success. Whatever the size of your company, it is imperative to start now evaluating the impact of these deadlines, understanding the necessary changes to your processes, and choosing appropriate solutions. Preparing in advance allows not only compliance with the law, but also transforming this constraint into an opportunity for optimization and modernization of your financial flows.

Anticipate Without Complexity: Strategies and Tools for Your Compliance

The electronic invoicing reform, with its e-invoicing and e-reporting components, can seem intimidating. However, a structured approach and wise technology choices allow you to anticipate these obligations without unnecessary complexity, even transforming the constraint into a lever for performance in your company.

A Structured Approach Beyond Pure Technology

The error would be to consider electronic invoicing solely as a technical challenge. In reality, it is first and foremost an organizational transformation. The first step is to conduct a complete internal audit of your current invoicing flows, both in emission and reception. Key questions to ask yourself:

- What are my volumes of domestic B2B invoices?

- What share of my activity falls under B2C or international operations?

- What are my current invoice formats? Are they already partially structured?

- How are my purchasing and sales processes managed, from order to payment?

- What information systems (ERP, accounting tools, CRM) are involved in these processes?

This analysis will enable you to design the target organization, identify potential bottlenecks, and define a clear roadmap. It is not simply a matter of replacing a manual process with an electronic process, but of rethinking the entire value chain to maximize benefits in terms of automation, reliability, and speed.

Distinct But Interoperable Tools: A Relevant Strategy

The administration does not constrain companies to use a single solution to manage all their e-invoicing and e-reporting obligations. On the contrary, it is often more pragmatic to adopt a modular approach, relying on specialized tools but capable of communicating with each other. Interoperability is the key. This reflection should guide the choice of your platform.

For example:

- Your ERP or invoicing tool can focus on issuing B2B electronic invoices and generating e-reporting data for your sales.

- A e-procurement or Procure-to-Pay (P2P) solution, like Weproc, can excel in managing the receipt of supplier invoices, their control, validation, and automated integration into your accounting. These solutions are particularly effective for managing volumes and securing the processing of incoming flows.

This division of roles allows you to exploit the best of each solution, while ensuring that data flows harmoniously between different systems via approved platforms. Flexibility is a major asset in an evolving regulatory environment.

The Separation of Emission/Reception Roles as a Lever

For many organizations, the separation of responsibilities between invoice emission and receipt is not only possible, but desirable. The sales department or business management typically handles invoice emission, while purchasing and accounting services manage receipt and processing of supplier invoices.

This approach offers several advantages:

- Security of compliance at receipt: It is often here that volumes are highest and risks of error greatest. A dedicated receipt solution, capable of verifying the compliance of incoming electronic invoices, automating reconciliation with orders and receipts, and managing validation workflows, is a guarantee of peace of mind.

- Less complexity for emission: By not requiring your invoicing system to manage the entire cycle, you simplify its e-invoicing compliance, reducing adaptation costs and timelines.

- Optimization of existing processes: Rather than overhauling everything, you can capitalize on the strengths of your current systems and add specialized building blocks for the most critical aspects of the reform.

Procure-to-Pay (P2P): A Lever for Overall Performance

The integration of e-invoicing and e-reporting into a complete Procure-to-Pay (P2P) approach represents an exceptional opportunity to transform a regulatory constraint into a strategic advantage. A P2P solution such as Weproc offers a unified and automated view of the entire purchasing and payment cycle, from purchase request to invoice accounting integration.

By integrating the management of electronic invoices and e-reporting data, P2P allows:

- Reliabilize data: Reduction of entry errors, automatic information validation, consistency between documents (orders, deliveries, invoices).

- Accelerate processes: Automation of validation workflows, elimination of manual tasks, reduction of payment and collection times, invoice receipt automation is a major advantage.

- Strengthen control: Better visibility into spending, real-time budget control, complete traceability of flows.

- Optimize cash flow: Proactive payment management, easier supplier negotiation.

- Ensure compliance: Guarantee that all incoming and outgoing invoices, as well as transmitted data, meet the legal requirements of e-invoicing and e-reporting.

The challenge is not only to be compliant, but to be so efficiently and profitably. A well-implemented P2P solution transforms electronic invoicing into a catalyst for more agile and performant financial management.

In conclusion of this journey into the heart of 2026 electronic invoicing, it is essential to reaffirm a capital distinction: e-invoicing and e-reporting, although often confused, are two distinct but complementary obligations that govern the dematerialization of commercial flows in France. E-invoicing, with its domestic B2B scope, aims to standardize and secure the exchange of complete invoices between professionals. E-reporting, for its part, ensures the transmission of transaction data to the tax administration for all other flows, whether B2C or international.

Understanding this nuance is not a simple semantic formality; it is the key to successful anticipation and flawless compliance. Ignoring one or the other of these obligations is to expose yourself to operational, financial, and reputational risks. The progressive timeline for 2026-2027 offers a window of opportunity, but it should not be a source of procrastination. All companies, regardless of size, are concerned and must actively prepare.

The digital transformation imposed by this reform should not be perceived as an isolated constraint, but rather as an essential component of a comprehensive modernization strategy. By adopting a structured approach, choosing interoperable tools, and capitalizing on proven solutions like Procure-to-Pay, companies can not only meet legal requirements, but also and above all, transform their financial and purchasing processes. They will gain in automation, data reliability, spending visibility, and ultimately, overall performance.

At Weproc, we are convinced that compliance with electronic invoicing is a unique opportunity to rethink and optimize your value chain. Our expertise and P2P solutions are designed to accompany you step by step in this transition, ensuring smooth integration of e-invoicing and e-reporting into your daily operations. Do not suffer the reform, use it as a lever to build a sustainable trajectory of compliance and financial control.